Understanding What Contractor Insurance is

Contractor insurance is a policy that protects contractors from financial loss resulting from accidents and negligence on the job. Insurance for contractors is important as it covers both the employer and employees from accidents, worker injuries, equipments, and workers’ compensation. Essentially, it covers any damages that are the fault of the contractor.

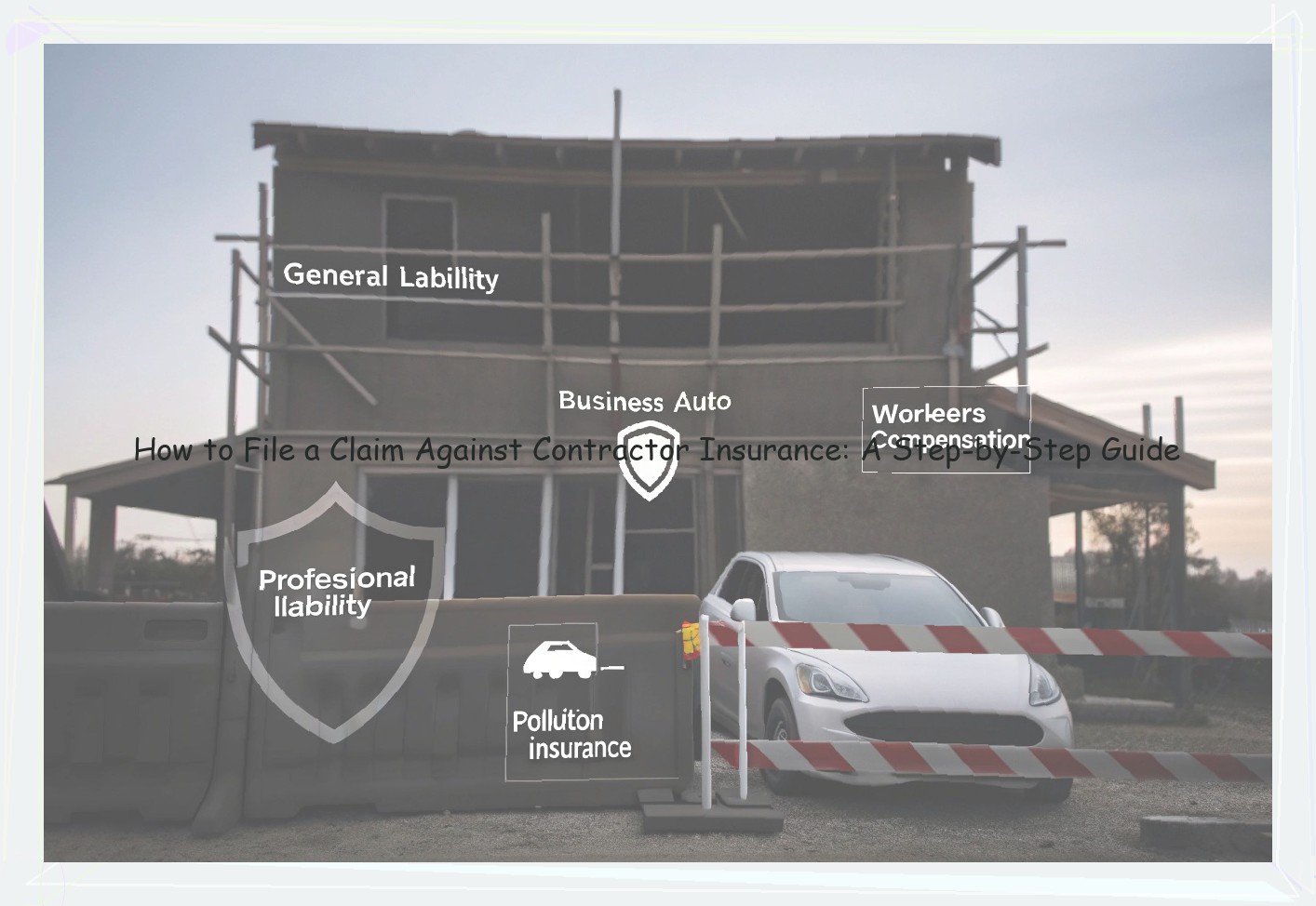

Depending on the type of coverage, the insurance can protect contractors from an array of possible problems on the worksite, such as;

General Liability Insurance

– Covers general third-party property damage and bodily injury to other people and any legal fees incurred in connection with these risks.

Automobile Insurance

– Business automobile policy covers vehicles used in the course of a business in addition to liability.

Workers Compensation Insurance

– Workers’ compensation insurance covers work-related injuries and illnesses.

Builder’s Risk Insurance

– Builder’s risk insurance protects against subsequent events that may happen to the construction site before it is turned over to the owner.

Contractors Professional Liability Insurance

– Errors and omissions coverage for claims made against design professionals , including architects, planners, and engineers. It covers damages related to harm from negligent professional services including over and under-designed buildings.

Pollution Insurance

– Begins when other contracts exclude pollution from coverage.

Business Owner’s Policy

– Business owner’s policy (BOP) offers several forms of coverage, like business personal property, which include items such as materials, equipment, tools, fixtures, and some furnishings related to your contracting business.

Professional Liability Insurance

– Also called Errors and Omissions insurance, it protects business owners from claims not related to bodily injuries that stem from mistakes or negligence.

Surety Bonds

– Surety bonds are not exactly insurance but are a third-party agreement that agrees to pay others-that oftentimes include disputes between contractors over work or behaviors of employees. It is also known as fidelity bonds for contractors.

Insurance for contractors is vital in case there is damage to your job site or to someone else’s property as well as for protection in case of a lawsuit.

Determining When You Need to File a Claim

Identifying When to File a Claim Against Contractor Insurance

When faced with the decision to file a claim against a contractor’s insurance policy, it is important to understand if the situation qualifies as a valid claim, as well as the potential risks involved. In some cases, the impact to the contractor may be severe enough that it could result in dissolution of their business. So there are obvious legal and financial implications for proceeding or not proceeding with a lawsuit, and this is something that should not be taken lightly. However, there are a few common situations where a claim on a property damage/malpractice policy may have merit; it is a good idea to familiarize yourself with those purposes and examples.

The most frequent reason for filing a claim against contractor insurance is to address physical damage to property. This could be damage to a home caused by the negligence of a subcontractor. It could also result from an accident on-site due to improper safety equipment or training, or a failure to adhere to the appropriate building codes. First after you suspect there has been damage as a result of the contractor’s work, you should contact your insurance agent and inform them of your suspicions. Then you will be guided through the claims process; your agent or the adjuster will likely meet you on-site in order to inspect the damage and determine what kind of coverage applies. If the damage for which you intend to file a claim is not of the physical nature, you may consult your agent to better understand if the damage is eligible for coverage. Common examples include: incomplete work, improper installation, or product defects.

Collecting the Necessary Documentation

When you make a claim against a contractor’s insurance policy, supporting documentation will prove vital for the success of your endeavor. Most types of property damage require proof that the loss stemmed from the actions or neglect of the contractor in question. Given the potential for ambiguity, dispute regarding liability abounds in contractor-customer transactions. As such, an unsuspecting contractor may find itself on the receiving end of a Channel 11 news reporter’s microphone after failing to provide a customer with a satisfactory product. Photos, receipts, contracts, and other pertinent paperwork allow the victimized customer to craft a compelling case against the contractor and ultimately receive a timely insurance settlement as a result.

Specifics may vary depending on the nature of the claimed loss and the terms of the contractor’s policy. In general, however, the relevant documents should include: When speaking with the contractor’s insurer, you will need to provide a detailed description of the problem. Unless required by law, most contractors have no obligation to retain documentation regarding the status of ongoing work. In turn, contractor files do not generally contain much information beyond that included in the contract itself, even if your contractor was validly insured. Therefore, you must accrue and provide as much detail as possible. Photographs of the damaged item — a roadway joint, brick fireplace, or recreational vehicle — will be most useful if they were taken prior to the execution of the contract. However, photographs of the damage may also suffice if retained immediately after damage occurred. Your contractor might attempt to convince you that photos of any stage of work will have little impact on your claim. Do not be persuaded too easily, as photographic evidence may make all the difference if your contractor attempts to paint you in a less than flattering light.

Filing a Claim

The process of filing a claim against contractor insurance typically begins with the homeowner reaching out to the insurance provider to alert them that they would like to file a claim. It is important to note that in most cases, those every those every purely verbal or written incidents of property damage should be documented and saved, in case a claim needs to be filed. Once the homeowner contacts the insurance provider to file a claim, the insurance company will most often assign an adjuster to visit the property on a scheduled date.

While the homeowner may have been inconvenienced for an extended period of time, there is nothing that they need to do to prepare for the visit from the adjuster. During the visit, the adjuster will ask that the homeowner be present to discuss any incidents that the homeowner believes may have been caused by the contractor’s work. This discussion should also include a thorough review of any damage that has occurred as a result of the incident. The adjuster will then take pictures and document any damage that they believe should be covered by the contractor’s insurance policy.

Next, the adjuster will contact the contractor’s insurance provider to determine the policy limits that may apply to the homeowner. Depending on the outcome of this discussion, the contractor’s insurance provider may fax or email a copy of the policy to the adjuster within a few days or weeks. In most cases, however, it can take several weeks or even longer for the contractor’s insurance provider to send a copy of the policy to the adjuster.

Typically, it takes anywhere from a few days to a month for the adjuster to receive a copy of the contractor’s insurance policy. Once the policy has been received and all damage has been documented, there are several potential outcomes. The first is that the adjuster determines that the contractor is not liable for the damages, and denies the claim. In this scenario, the homeowner would be responsible for the costs associated with restoring the property. The second outcome is the complete opposite of this scenario. If the contractor is found to be entirely responsible for the damages and agrees to accept responsibility, they and their insurance company will issue a check to the homeowner, and will then provide instructions on how they should use the funds.

The third outcome is the most likely based on experience, and it is an partially favorable decision for the homeowner. This outcome means that the contractor and their insurer are only willing to pay some of the amount that is needed to restore the property. If this is the case, both the contractor and the homeowner must reach a compromise and agreement on which party will be responsible for certain costs.

Common Roadblocks and How to Avoid Them

When making a claim against a contractor’s insurance policy, homeowners may face a number of common challenges that they should be prepared to overcome. One such challenge is understanding the language used by insurance adjusters, which can be laden with industry-specific jargon or ambiguous terms that are not easily understood. It is helpful to ask the adjuster to clarify terms that are unfamiliar and to seek legal advice if there is any confusion or suspicion that the adjuster may be trying to downplay the scope of damages.

Another common challenge is the voluminous amount of paperwork required for a claim. Homeowners are encouraged to keep thorough records, including photographs and detailed accounts of communication with the contractor and adjusters. This can be time consuming but is essential in the event of a dispute as to the extent of damages or the cause of the loss.

Homeowners may also encounter resistance when seeking compensation for intertwined issues in a home , such as fire and water damage from an associated fire suppression system leak. Insurance companies may attempt to minimize claims by decreasing the repair estimate or attempting to assign blame for water damage to the fire suppression system leak rather than the fire itself. It is important to provide a full accounting of damages, as well as evidence of how the problems are inextricably linked, to maximize the chances of a successful claim.

Finally, the claim process can be lengthy and frustrating as results may not be immediate. Homeowners should remain calm and persistent. Keep in mind that the insurer is obligated to make a fair and honest settlement offer. If they fail to do so, even after negotiation attempts, they can be held legally liable. Homeowners can also request a review of their claim by a neutral third-party umpire, as provided by most insurance policies, to facilitate their recovery.

Legal Counsel and Expert Assistance

Some contractor insurance policy disputes can be complicated, or have some unusual circumstances, or simply be at an impasse. Sometimes simply having a claim denial review done by someone experienced with contractor insurance policies and claims can help smooth the way. And sometimes consulting with an attorney can really help explain your options going forward in a complicated situation.

As always, reading this blog (or any other lawyer blog) does not create an attorney-client relationship. No attorney-client relationship is established until you personally sign an agreement with an attorney.

These matters can be complex and don’t lend themselves well to "blogging it". If you feel that a claim, or a claim denial, is complex, you should seriously consider hiring an attorney or claims consultant to look at it on your behalf. Sometimes, all that is required is experience looking at similar situations. Other times, if you have a case where you are owed money and the builder has closed down shop, you might need an attorney to go after a compliance bond. Other other times you might need supplemental proceedings commenced to stop a builder from absconding with your money improperly. And often, the various construction codes and statutes should carefully be considered.

I’ve had experience with bonds, bond claims, bond recoveries, supplemental proceedings, insurance policy disputes, Insurance Benefits Review (IBR), and more. It’s important to note that if a serious situation comes about, you may need to hire a contractor insurance lawyer.

Prevention and Tips for Future Projects

In advance of contracting work to be performed, a homeowner or a project manager should include a number of protective clauses in their contract with the contractor set forth below:

A. Warranties. Inclusion of details regarding the warranties provided by the contractor for the work to be performed, and the process to claim under such warranties.

B. Dispute Resolution. Include a detailed dispute resolution clause requiring the parties to submit any disputes to mediation prior to filing any action in court. Such a clause can require the parties to work with a specifically selected mediator , or allow the parties to select the mediator from a panel that is acceptable to both parties.

C. Choice of Law. Set forth what law shall apply to the interpretation of the contract. It is suggested that this clause provide the laws of New York only to apply if the parties are unable to mutually agree on a different state whose laws should control.

D. Written Contracts. Require that all changes to the work agreed to by both parties be in writing. While there is an exception in New York where a party may be able to make a claim based upon an "implied contract" where a party fails to pay for the services provided, including this clause may save the professionals time and money if they have to litigate the fees and costs associated with the performance of the work under the contract.